Frugal living is a lifestyle choice that prioritizes mindful spending, productivity and simplicity. It best sounds with anyone looking to better manage their finances and want to live a life aligned with their values. Frugal living is not about poverty, it is about making smart, intentional decisions to maximize value and minimize waste. By embracing this mindset, you can save money, enjoy greater financial stability, and still taste life joys.

In this blog post, we’ll explore the benefits of frugal living, share everyday habits to cut costs, and discuss the long-term financial advantages of adopting a frugal mindset. Plus, we’ll provide 25 tips to save money for frugal living.

Benefits of frugal living

Frugal living is not just about saving a few dollars here and there, it is about creating a sustainable lifestyle that aligns with your financial goals. Here are some key benefits:

Financial stability: Frugality helps you build an emergency fund, pay off debt, and save for future goals.

Reduced Stress: Knowing your finances are under control can give you peace of mind.

Minimalist living: By focusing on essentials, you reduce your confusing mindset and prioritize what truly matters.

Environmental Sustainability: Frugal choices often lead to less waste and a smaller carbon footprint.

Increased Freedom: With fewer financial burdens, you can pursue passions and experiences without worry.

Everyday Habits to Cut Costs

These small yet consistent changes in your daily routine can add up to significant savings. Here are some practical habits to adopt:

Create and Stick to a Budget: A budget is the foundation of frugal living. It helps you to track spending and allocate money to priorities.

Plan Meals and Shop Smart: Meal planning reduces food waste and prevents impulse purchases. Stick to a grocery list to stay on track.

DIY Projects: From home repairs to crafting gifts, doing things yourself can save money and boost creativity.

Cut Unnecessary Subscriptions: Review streaming services, gym memberships, and other recurring expenses. Cancel what you don’t use.

Buy Secondhand: Thrift stores, consignment shops, and online marketplaces offer affordable alternatives for clothing, furniture, and more.

Use Cashback and Coupons: Apps like Rakuten or Honey help you save money on purchases, while coupons provide instant discounts.

Practice Minimalist Budgeting: Focus on needs over wants and prioritize quality over quantity in your spending.

Repair Instead of Replace: Fixing items such as clothing, appliances, or electronics can save money and reduce waste.

Switch to Energy-Efficient Practices: Use LED bulbs, unplug devices when not in use, and adjust your thermostat to lower utility bills.

Embrace Free Entertainment: Visit parks, attend community events, or borrow books and movies from the library.

Long-Term Financial Advantages of a Frugal Mindset

Adopting a frugal lifestyle is not just about short-term savings. it is a pathway to long-term financial security. Here’s how:

Debt reduction: Frugal habits free up funds to pay off loans and credit card balances faster.

Wealth building: By spending less, you can invest more in savings accounts, retirement funds, or other financial vehicles.

Emergency preparedness: A frugal lifestyle helps you to build an emergency fund, providing a safety net for unexpected expenses.

Financial independence: With reduced expenses, you’ll need less income to sustain your lifestyle, paving the way to early retirement or flexible work options.

Borrow books, tools, or equipment instead of buying.

Opt for no-contract phone plans to lower monthly bills.

Turn off lights and unplug devices when not in use.

Choose generic brands over name brands.

Make coffee at home instead of buying it daily.

Set clear savings goals to stay motivated.

Delay non-essential purchases for 24 hours.

Unsubscribe from marketing emails to reduce spending temptations.

Batch cook and freeze meals for busy days.

Explore free or low-cost local entertainment.

Negotiate better rates for utilities, internet, or insurance.

Use public transportation or carpool to save on gas.

Repair damaged items instead of replacing them.

Build a 3-6 month emergency fund.

Simplify your wardrobe with versatile pieces.

Avoid credit card debt by paying in full each month.

Start a small garden to grow your own food.

Practice gratitude to shift focus from material possessions to meaningful experiences.

Final Thoughts

Frugal living is far more than a money-saving strategy. It is a way to reclaim control over your finances and live with confidence. By incorporating these tips and adopting a minimalist mindset, you can reduce expenses, achieve financial goals, and enjoy a more intentional, fulfilling life.

Remember, frugality isn’t about restriction. It is about making your money work for you. Start small, stay consistent, and watch as the benefits of frugal living transform your life.

Economical uncertainty is uncertain, and a recession is one of the most significant events that can impact your personal finances. Let’s face it—recessions are stressful. The thought of job losses, shrinking savings and economic uncertainty can keep anyone up at night. But here’s the thing, while you can’t control the economy, you can control how prepared you are. With the right steps, you can protect your finances and face a recession with confidence.

In this guide, I’ll walk you through a step-by-step plan to prepare for a recession. Whether you’re just starting to think about it or already taking action, these tips will help you build a solid financial safety net. Let’s get started!

What is a Recession?

A recession is when the economy slows down significantly. This slowdown impacts various aspects of the economy, including employment, production, and spending. Typically, recession last for several months, but they can vary in duration and severity. It’s important to understand that recession is a normal part of the economic cycle and they usually follow a period of economic expansion.

For everyday individuals, the effects of a recession can include job losses, reduced wages and a decrease in the value of investments. Essentially, during a recession, businesses make less money, and in turn, they reduce their workforce or cut expenses.

What is the difference between recession and Depression?

Recession

Think of a recession as a temporary but significant dip in the economy. It could be caused by various factors, including a sudden decline in consumer demand, financial crises or shifts in policy (like higher interest rates). Recession typically last for a few months to a year or so. During a recession, people experience job losses, businesses close, and stock markets dip. However, with appropriate economic intervention (like stimulus packages), recovery usually occurs.

Depression

A depression is far more severe and long-lasting. It is marked by an extended period of economic decline, often spanning years rather than months. The effects are deeper and can involve widespread unemployment, massive bankruptcies, and prolonged financial hardship. The Great Depression, which began in 1929, is the classic example of a depression that lasted for over a decade and affected many countries worldwide.

Understanding the difference is important because a recession, while tough, is not as long-lasting or devastating as a depression.

What typically happens in a recession?

During a recession, the economy experiences various challenges:

Increased Unemployment: Businesses like retail, travel, and hospitality, may cut down on staff due to reduced consumer spending. This leads to higher unemployment rates, making it harder for people to find jobs.

Decrease in Consumer Spending: People are less likely to make major purchases during a recession, which directly affects businesses. This can lead to a cycle of more layoffs and slower economic recovery.

Stock Market Volatility: Investors tend to panic when they see negative economic indicators. As a result, stock markets experience sharp declines as people sell off their assets to minimize risk. This can affect individual investors’ retirement accounts and savings.

Business Failures: Smaller businesses may not have the financial cushion needed to survive during a recession. Without steady cash flow and with reduced customer demand, many businesses could close their doors.

Falling Property Values: In a recession, people might hold off on buying homes or invest less in property. This causes housing markets to slow down, often resulting in reduced property values and fewer transactions.

How to prepare yourself for a recession

Preparing for a recession isn’t just about saving money—it’s about positioning yourself for financial stability during challenging times. Here’s a deeper look into each strategy:

Step 1: Build an emergency fund

An emergency fund is your financial lifeline during tough times. It’s the money you set aside to cover unexpected expenses, like a job loss or medical bill.

How much should you save? Aim for 3-6 months’ worth of living expenses. If that feels overwhelming, start with a smaller goal, like $1,000.

Where should you keep it? Store your emergency fund in a high-yield savings account. It’s safe, earns interest, and is easy to access when you need it.

Pro Tip: Automate your savings. Set up a monthly transfer to your emergency fund so you’re consistently building it without even thinking about it.

Step 2: Reduce your debt

Debt can feel like a heavy weight during a recession. The less you owe, the more financial freedom you’ll have.

Focus on high-interest debt first. Credit cards and payday loans often have the highest interest rates, so tackle those first.

Consider debt consolidation. If you have multiple debts, combining them into one lower-interest loan can make repayment easier.

Avoid new debt. Pause unnecessary purchases on credit and stick to a budget.

Step 3: Diversify Your income

Relying on a single source of income is risky during a recession. Diversifying your income can provide stability and peace of mind.

Start a side hustle. Freelancing, tutoring or selling handmade goods online are great options.

Invest in passive income. Consider dividend-paying stocks, rental properties, or creating digital products like eBooks or courses.

Upskill. Learn new skills that can make you more employable or open up new income opportunities.

Step 4: Cut unnecessary expenses

Take a hard look at your spending habits. Cutting back on non-essentials can free up cash to boost your savings or pay off debt.

Track your spending. Use apps like Mint or YNAB to see where your money is going.

Trim the fat. Cancel unused subscriptions, dine out less, and shop smarter by using coupons or buying in bulk.

Focus on needs vs. wants. Ask yourself, “Do I really need this?” before making a purchase.

Step 5: Review and Adjust your investments

A recession can hit your investments hard, but a well-balanced portfolio can help you weather the storm.

Diversify your investments. Don’t put all your eggs in one basket—spread your money across stocks, bonds, and other assets.

Avoid panic selling. Market downturns are temporary and selling during a dip can lock in losses.

Consult a financial advisor. If you’re unsure about your investment strategy, seek professional advice.

Step 6: Boost your job security

In uncertain times, it’s smart to make yourself indispensable at work.

Excel in your role. Go above and beyond to show your value to your employer.

Expand your skills. Take online courses or certifications to make yourself more versatile.

Network. Build relationships within your industry so you have a support system if you need to find a new job.

Step 7: Stock up on essentials

During a recession, prices for everyday items can rise. Stocking up on essentials can save you money in the long run.

Buy non-perishable items. Think canned goods, toiletries and cleaning supplies.

Shop sales and use coupons. Stock up when items are discounted.

Don’t overdo it. Only buy what you’ll actually use to avoid waste.

Step 8: Protect your credit score

A good credit score can be a lifesaver during tough times, especially if you need to take out a loan or refinance.

Pay bills on time. Late payments can hurt your score.

Keep credit card balances low. Aim to use less than 30% of your available credit.

Check your credit report. Look for errors and dispute them if necessary.

Step 9: Stay informed but avoid panic

It’s important to stay updated on economic trends, but don’t let fear drive your decisions.

Follow trusted news sources. Stick to reputable outlets for accurate information.

Limit exposure to doom-and-gloom headlines. Too much negativity can lead to unnecessary stress.

Focus on what you can control. Instead of worrying about the economy, focus on taking actionable steps to protect yourself.

Step 10: Create a long term financial plan

Preparing for a recession isn’t just about surviving—it’s about thriving in the long run.

Set financial goals. Whether it’s buying a home, retiring early or starting a business, having clear goals keeps you motivated.

Review your budget regularly. Make adjustments as needed to stay on track.

Stay disciplined. Even when times are good, stick to your financial plan to build lasting security.

Mistakes to Avoid During a Recession

Even with the best preparation, it’s easy to make some common mistakes during a recession:

Panic Selling Investments: If the stock market crashes, it is tempting to sell off investments in a rush to avoid further losses. However, selling in a panic often locks in your losses. Instead, focus on long-term goals, and don’t let short-term volatility dictate your actions.

Neglecting Your Emergency Fund: It’s tempting to dip into your emergency fund for non-essential expenses during tough times. However, your emergency fund should be used only for true emergencies like medical bills, essential home repairs, or temporary unemployment. Keep this money intact so it can help you when you truly need it.

Ignoring Your Debt: You may be tempted to stop paying off your debt if you are financially stressed during a recession. But neglecting debt can hurt your credit score and lead to higher interest payments in the future. Prioritize paying off high-interest debts first, such as credit cards, to avoid accumulating more financial stress.

Cutting Back Too Much: While it’s important to reduce expenses, be careful not to sacrifice too much. For example, avoiding preventative medical care or skipping meals to save money can hurt your health. Balance your budget cuts with your well-being, and ensure you’re still living a healthy, sustainable lifestyle.

Conclusion

Recessions are a natural part of the economic cycle, but they don’t have to derail your life. By following these steps, you can protect your finances, reduce stress, and come out stronger on the other side.

Remember, preparation is key. Start today—even small actions can make a big difference.

What’s your #1 tip for preparing for a recession? Share it in the comments below! And don’t forget to subscribe for more practical financial advice.

Managing finances as a couple can be both rewarding and challenging. Whether you’re saving for a dream vacation, planning to buy a home, or simply trying to avoid arguments over spending habits, budgeting apps can be a game-changer. In 2025, the world of financial technology has evolved, offering couples more tools than ever to streamline their money management.

This comprehensive guide will walk you through everything you need to know about best budget apps for couples, from why they’re essential to how to choose the right one for your relationship. We’ll also explore topics that other blogs haven’t covered, ensuring you have all the information you need to take control of your finances together.

Why To Need The Best Budget Apps For Couples

The Challenges of Managing Finances as a Couple

Let’s face it—money is one of the most common sources of conflict in relationships. Differing spending habits, unequal incomes, and a lack of transparency can lead to misunderstandings and stress. Without a clear system in place, it’s easy to lose track of shared expenses, miss bill payments, or fail to save for future goals.

The Benefits of Using The Best Budget Apps for Couples

Budgeting apps are designed to simplify financial management by providing tools that promote transparency, collaboration, and accountability. Here’s how they can help:

Real-Time Updates: Both partners can see transactions and account balances instantly.

Shared Accountability: Tracking spending together encourages responsible financial behavior.

Collaborative Goal Setting: Apps make it easy to set and achieve shared financial goals, like saving for a house or paying off debt.

How Budgeting Apps Strengthen Relationships

By fostering open communication and reducing financial stress, budgeting apps can actually strengthen your relationship. When both partners are on the same page about money, it’s easier to focus on building a life together.

Key Features to Look for in Budget Apps for Couples

Not all budgeting apps are created equal. Here are the features you should prioritize when choosing one for your relationship:

1. Shared Accounts and Real-Time Syncing

The best budget apps for couples should allow both partners to link their accounts and view transactions in real time. This ensures transparency and makes it easier to track shared expenses.

2. Expense Tracking and Categorization

Look for apps that automatically categorize expenses, so you can see where your money is going. This is especially useful for identifying areas where you can cut back.

3. Bill Reminders and Alerts

Never miss a payment again! Apps with bill reminders and alerts help you stay on top of due dates and avoid late fees.

4. Financial Goal Setting

Whether you’re saving for a wedding, a vacation, or a down payment on a house, your app should help you set and track financial goals.

5. Ease of Use and Compatibility

A user-friendly interface and cross-platform compatibility are essential. After all, you don’t want to spend hours figuring out how to use the app.

6. Security and Privacy

Your financial data should be protected with robust security measures, such as encryption and two-factor authentication.

Top Best Budget Apps For Couples in 2025

1. Monarch money

Monarch money budgeting app is spatially designed for couples who value detailed insights into their finances. It allows both partners to log in with individual credentials, ensuring privacy while maintaining a shared financial overview. Monarch syncs with over 11,000 financial institutions, pulling in data from bank accounts, loans, and credit cards to provide a comprehensive picture of your financial health.

Why Couples Love It:

User-friendly dashboards for tracking expenses.

Customizable budgets for shared and individual goals.

Seamless integration with financial accounts.

Best For:

Couples who are detail-oriented and want in-depth financial analyses.

Honeydue is specifically designed with couples in mind. The app allows you to share selected financial information—such as bank accounts, credit cards, and loans, while keeping certain details private if needed. It is an excellent tool for tracking expenses, setting shared budgets, and ensuring transparency in your financial journey.

Why Couples Love It:

Customizable account sharing settings.

Alerts for upcoming bills to avoid missed payments.

Support for over 20,000 financial institutions across multiple countries.

Best For:

Couples who want to balance transparency with privacy.

You Need a Budget, or YNAB, takes a proactive approach to budgeting. Using the zero-based budgeting system, it encourages users to assign every dollar a job. YNAB offers real-time syncing between devices, making it easy for couples to stay on the same page about their financial priorities.

Why Couples Love It:

Real-time updates for shared expenses.

Goal-setting features for short- and long-term objectives.

Extensive educational resources to improve financial literacy.

Best For:

Couples who want a structured, hands-on budgeting system.

Goodbudget brings the classic envelope budgeting method into the digital age. This app allows couples to allocate money into virtual envelopes for different spending categories, making it easy to visualize where your money is going. It’s a great choice for those who prefer a straightforward approach to budgeting.

Why Couples Love It:

Simple envelope-based system for expense tracking.

Easy-to-share budgets for collaborative financial management.

Reports that provide insights into spending habits.

Best For:

Couples who prefer simplicity and a visual budgeting method.

Albert is more than just a budgeting app; it’s a full-fledged financial assistant. Couples can use it to track expenses, manage shared budgets, and even receive personalized advice from human financial experts. Albert also offers investment options and identity protection, making it a versatile tool for couples looking to manage their finances comprehensively.

Why Couples Love It:

Personalized financial advice tailored to your goals.

Automatic savings features to help you reach milestones faster.

Options for investment and cash flow management.

Best For:

Couples who want an all-in-one solution with expert guidance.

How to Choose the Right Budget Apps for Your Relationship

With so many options available, choosing the right budgeting app can feel overwhelming. Here’s a step-by-step guide to help you decide:

1. Assess Your Financial Goals

Are you saving for a big purchase, paying off debt, or simply tracking expenses? Different apps cater to different needs, so it’s important to choose one that aligns with your goals.

2. Consider Your Budgeting Style

Do you prefer automated tracking or manual input? Some apps, like YNAB, require more hands-on effort, while others, like Mint, automate most of the process.

3. Evaluate Compatibility

Make sure the app works on both partners’ devices and integrates with your bank accounts.

4. Test the App

Take advantage of free trials or basic versions to see if the app meets your needs before committing.

5. Discuss as a Couple

Budgeting is a team effort, so it’s important that both partners are comfortable with the chosen app.

Tips for Using Budgeting Apps Effectively as a Couple

1. Set Clear Financial Goals Together

Define short-term and long-term objectives, such as saving for a vacation or paying off student loans.

2. Schedule Regular Money Check-Ins

Set aside time each week or month to review your budget, track progress, and make adjustments as needed.

3. Be Transparent About Spending

Avoid financial secrets and build trust by being open about your spending habits.

4. Celebrate Milestones

Acknowledge achievements, like paying off a credit card or reaching a savings goal, to stay motivated.

5. Adapt as Your Needs Change

Your financial situation will evolve over time, so be prepared to update your budgeting strategy accordingly.

6. Tax Planning for Couples

Budgeting apps can also help you prepare for tax season by tracking deductible expenses, charitable donations, and other tax-related items.

Frequently Asked Questions (FAQs)

Are budgeting apps safe to use?

Yes, most budgeting apps use encryption and other security measures to protect your financial data. However, it’s important to choose a reputable app and use strong passwords.

Can unmarried couples use these apps?

Absolutely! Many budgeting apps, like Zeta, are designed with unmarried couples in mind.

What if one partner is reluctant to use a budgeting app?

Start by having an open conversation about the benefits of budgeting together. You can also suggest trying a free app or starting with a simple system.

Are there free budgeting apps for couples?

Yes, apps like Mint and Honeydue offer free versions with basic features.

How do I switch from one budgeting app to another?

Most apps allow you to export your data, making it easy to switch to a new platform. Be sure to review the new app’s features and compatibility before making the switch.

Conclusion

In 2025, budgeting apps have become an indispensable tool for couples looking to manage their finances effectively. By choosing the right app and using it consistently, you can reduce financial stress, achieve your goals, and build a stronger relationship.

Take the first step today by exploring the apps mentioned in this guide and discussing your financial goals with your partner. Remember, budgeting is a journey—not a destination. With the right tools and mindset, you can create a brighter financial future together.

In 2025, artificial intelligence (AI) is set to transform the financial industry in unprecedented ways. From personal finance management to investment strategies, AI is making it easier for individuals and businesses to manage, invest, and grow their money with smarter ai finance tools and more personalized services. Whether you are a beginner or a seasoned investor, the following five best AI finance tools are changing the way people handle their finances, helping users to save time, make better decisions, and optimize their financial strategies.

Wealthfront (AI-Powered Robo-Advisor)

Overview:

Wealthfront is one of the best AI finance tools that has been a leading robo-advisor for several years, but in 2025, it Is using advanced AI to offer more personalized financial advice. It automates the investment process and uses AI to create customized investment portfolios based on your financial goals, risk tolerance, and time horizon.

Key Features:

Personalized Investment Plans: Wealthfront’s AI analyzes your spending habits and savings behavior to recommend tailored investment strategies.

Tax-Loss Harvesting: Wealthfront uses AI to automatically sell losing investments to offset gains, minimizing your taxable income.

Financial Planning Tools: Its AI helps you set long-term goals, like saving for retirement or buying a home, and provides actionable steps to achieve them.

Why It’s Great for 2025:

Wealthfront AI finance tool ensures that your portfolio is constantly optimized for market changes, offering a hands-off approach to investing. It allows users to grow their wealth while minimizing the risks involved with human error.

Mint (AI-Powered Budgeting and Expense Tracking)

Overview:

Mint is one of the most popular budgeting apps. Mint app integrates AI to help users to understand their financial habits and improve their money management strategies. The app tracks your expenses, categorizes transactions, and provides personalized insights where you can save more.

Key Features:

Smart Budgeting: AI-powered suggestions that help you set achievable budgets based on past spending patterns.

Automatic Categorization: AI recognizes spending trends and automatically categorizes your transactions, so you can see exactly where your money is going.

Financial Insights: Mint’s AI offers tips on saving, investments, and credit management based on your financial behavior.

Why It’s Great for 2025

Mint AI not only helps you track your finances but also analyzes them to provide real-time recommendations. Whether you need to save more or pay off debt faster, Mint AI-driven insights will help you achieve your financial goals.

Clearscore (AI-Driven Credit Monitoring and Financial Health Tool)

Overview:

Clearscore uses AI to help users monitor and improve their credit scores. By analyzing their financial history, AI suggests steps user can take to improve your credit score, such as paying off debt or adjusting spending habits.

Key Features:

Personalized Credit Advice: AI provides actionable insights into how users can improve their credit score by analyzing their credit report.

Credit Monitoring: Continuous AI monitoring alerts users to any significant changes in their credit report or new credit activities.

Customized Financial Products: Clearscore uses AI to recommend credit cards, loans, and other financial products that fit your credit profile.

Why It is Great for 2025

AI-powered credit scoring and monitoring tools help users take proactive steps toward improving their credit health. Clearscore offers personalized financial advice and updates, making credit management easier and more accessible.

Upstart (AI-Driven Personal Loans)

Overview

Upstart uses AI to streamline the lending process, offering personal loans with better rates than traditional credit scoring systems. By analyzing over 1,000 variables, including education and employment history, AI predicts the likelihood of repayment, which results in more accurate lending decisions.

Key Features:

AI-Based Loan Approval: AI reviews non-traditional data points to determine a borrower’s creditworthiness, making it easier for people with less-than-perfect credit to qualify for loans.

Lower Interest Rates: AI algorithms are designed to offer lower interest rates to borrowers who might otherwise be overlooked by traditional lenders.

Flexible Loan Terms: AI helps determine the best loan repayment terms based on the borrower’s financial situation.

Why It’s Great for 2025: Upstart’s AI-driven lending platform provides a more inclusive and efficient approach to personal loans. It eliminates the bias found in traditional credit scoring models and ensures that more people have access to financial products at competitive rates.

Zerodha (AI-Powered Stock Trading and Investment Platform)

Overview

Zerodha, one of India’s largest stock trading platforms, integrates AI to help investors optimize their portfolios. Zerodha AI finance tools analyze stock market trends and offer real-time insights into the best stocks to buy, sell, or hold, enabling smarter trading decisions.

Key Features:

AI-Based Stock Recommendations: The platform uses AI to analyze real-time market data and suggest stocks based on your trading style and preferences.

Smart Portfolio Management: AI helps track your portfolio’s performance and suggests rebalancing strategies based on market conditions.

Risk Management: The platform’s AI models continuously evaluate your investment risk and offer strategies to mitigate potential losses.

Why It’s Great for 2025

Zerodha AI-driven platform helps both beginners and experienced investors make informed decisions. With market conditions changing rapidly, having AI on your side ensures your trades are based on data-driven insights and up-to-the-minute trends.

Here is the complete pdf on Best AI finance tools 2025

Conclusion

The integration of AI into finance tools is revolutionizing how we manage money, invest, and plan for the future. In 2025, these AI-powered tools—Wealthfront, Mint, Clearscore, Upstart, and Zerodha—are at the forefront of making personal finance management easier, more efficient, and more accessible. Whether you’re looking to optimize your investments, improve your credit score, or streamline your budgeting process, these tools leverage the power of AI to help you make smarter, data-driven financial decisions.

As AI continues to evolve, we can expect even more advanced features and innovations in the financial space, empowering individuals and businesses alike to make better financial choices.

With the rise of technology, most of the people want to earn extra income from mobile to take advantage of technology. Whether you are saving for a special purchase, looking to build an emergency fund, or just want to increase your income, money making apps can be a great way to reach your financial goals. In this article, we’ll explore some of the best money making apps of January 2025, helping you to discover platforms that are not only reliable but also easy to use.

1. Swagbucks money making app

Swagbucks has been the best earning app for some past years and it will continue to shine in 2025 as well. This app allows users to earn points, known as “SB” by completing simple tasks such as watching videos, taking surveys, shopping online, and even playing games.

Why Swagbucks?

Multiple earning methods

User can earn money by taking surveys, shopping online, watching videos, and more.

Flexible rewards

Your can get cashback using PayPal cash or gift cards from popular retailers.

Uber is one of the best money making apps especially if have a car. As a rideshare driver, you can set your own hours, making it a flexible side hustle for anyone with a busy schedule.

Benefits of driving with Uber

Flexible schedules

It offers flexible schedule so that you can drive only when you are free.

Surge pricing

Your can earn more during peak hours or in high demand situations.

Weekly payouts

you can get paid quickly and directly to your bank account.

Rakuten also known as Ebates, helps you to earn cashback on every purchase from thousands of retailers. If you are already shopping online, this app can help you save money and earn extra cash simultaneously. If you wants to maximize saving this app can help you.

Advantages of Rakuten

Earn cashback from over 2,500 stores, including Amazon, Target, and Walmart.

If you love photography, this app is best for you. Foap offers a way to monetize your images. The app lets users to upload high quality photos they have taken. whenever someone purchases the image, the photographer earns a cut of the sale.

If you prefer earning money through physical work, TaskRabbit is an excellent app. It connects people who are willing to tasks individually. Whether it’s assembling furniture, running errands, or cleaning, TaskRabbit offers plenty of opportunities for people who enjoy hands-on work.

Shopkick is another rewards app that lets the users earn points for shopping, both in-store and online. Points (called “kicks”) are awarded for walking into stores, scanning product barcodes, making purchases, or shopping online through the app. You can redeem your kicks for gift cards or PayPal cash.

Upwork is one of the best freelancing platforms available, offering opportunities for professionals across various fields, including writing, graphic design, programming, and digital marketing. If you have skills you can utilize it on Upwork by working with international clients.

Benefits of Upwork

Find short-term projects or long-term freelance contracts.

Not all money making apps are created equal, and the best choice depends on your skills, schedule, and income goals. Here’s a quick guide to help you decide:

For passive income: Rakuten.

For active work: Uber, TaskRabbit, or Upwork.

For creative talents: Foap or Upwork.

For surveys and quick tasks: Swagbucks.

Conclusion

The top 7 money making apps of January 2025 prove that there’s an option for everyone, whether you’re looking for active gigs, passive income, or simple tasks. By adopting these apps, you can turn your spare time into earnings or even build a massive side hustle. Try out one (or more!) of these apps today to start maximizing your income potential.

Before now managing your finance was very difficult. But now in modern age it becomes manageable. By the use of best budgeting apps your smart phone is your personal finance manager. Budgeting apps have so many features which simplifies your financial management such as track your spending, set your goals and even suggests the ways to save money. As we take a step into 2025, here the most widely used 7 budgeting apps that can be your personal budget planner apps in 2025. Lets dive in.

1) YNAB (you need a budget)

YNAB is always on the top of the charts because of its personal finance philosophy. It is more than just a budgeting apps because it works on the principle of zero-based budgeting (In zero-based budgeting every dollar is assigned a job so that the personal have full control over his spending).

Features of YNAB

There are so many features of YNAB to focus but here we discuss few important features of YNAB.

Zero-based budgeting approach

Every dollar is assigned a job so that you can track every dollar.

Real time syncing with banks

This app syncs with your bank accounts that allows you to track your real time transaction.

Goal tracking

YNAB allows you to set your goals and track them , whether it is saving for an emergency , paying off debt, retirement savings or building savings for a large purchase.

Reports and insights

With this feature you can have detailed financial reports that give you insights to your spending habits which will helps you to adjust your budget accordingly.

This budgeting app is best for those who wants to invest time in deep learning finance as it has detailed budgeting strategy.

Pricing

Monthly plan : $14.99 USD*/month

Annual Plan : $9.08 USD*/month

or see the real time pricing details from their website.

2) Mint app

The mint budgeting app is the second best option after YNAB . It is especially made for beginners who want to automate their financial management. Mint budgeting app automatically categorizes your transactions and provide you clear and detailed insights to your spending habits. It offers you more passive approach to budgeting by tracking what you have spent and automatically compare it with your set limit. Mint budgeting app includes simple goal-setting features for saving or paying off debt. It tracks progress automatically as you spend and save.

Features of Mint budgeting app

Mint budgeting app has many features which beginners wants in personal finance app. here we discuss some important features.

Account Aggregation

Users can link multiple financial accounts, such as bank accounts, credit cards, loans and investments to view all their financial information in one place.

Budgeting Tools

Mint app offers users to create budgets, track spending across various categories and receive alerts when the user might approaching or exceeding budget limits.

Bill Tracking

Mint app provide reminders for upcoming bills which help users to avoid late fees and manage payments effectively.

Spending Insights

Mint app analyze spending patterns, offers insights and visualizations to help users understand their financial habits.

Goal Setting

Mint app enable users to set and track their financial goals, such as saving for a vacation or paying off debt.

Investment Tracking

Mint app provide tools to monitor investment accounts and portfolio performance.

This is the interface of Mint budgeting app

Best for

Mint app is best budgeting app for those who are looking for free, automated budget planner app to track all their financial accounts in one place. From creating budgets to monitor spending wisely. It’s ideal for users who prefer simplicity and real-time financial insights without much manual input.

EveryDollar budgeting app is also based on zero-based budgeting but follows Dave Ramsey’s principle. It is particularly the baby steps system, which prioritizes paying off debt and building an emergency fund. It is a bit more focused on goal-based financial planning. The EveryDollar and YNAB have many similarities but EveryDollar offers free version in which user can manually input all transactions to manage finance.

Features of EveryDollar

Zero-Based Budgeting

EveryDollar uses Dave Ramsey’s zero-based budgeting approach, where every dollar you earn is assigned a purpose, which helps you to track your spending.

User-Friendly Interface

EveryDollar offers clean and user friendly UI for their users to manage their personal finance.

Manual and Automatic Tracking

In the free version, you can manually enter your expenses, while the premium version automatically syncs with your bank accounts to track transactions automatically.

Customizable Categories

EveryDollar app adjust your budget to fit with your lifestyle by adding and organizing categories like groceries, entertainment, and savings goals.

Integration with Ramsey+

Premium users of EveryDollar app get access to additional resources like Financial Peace University and other tools that support Dave Ramsey’s financial principles.

This an interface of EveryDollar budgeting app

Best for

EveryDollar app is perfect for anyone who is looking for a straightforward and clean budgeting app that takes control of your money and reaching financial goals.

Pricing

Free version available and premium starts at 12.99USD /per month.

Honeydue app is best budget app for couples who wants to manage their finances together. This app allows partners to link their bank accounts, credit cards, loans, and bills in one place, making it easy to track spending, set budgets, and stay on the same page financially. The app offers features like customizable spending categories, bill reminders, and private or shared account views to respect individual privacy while fostering transparency. Honeydue app is perfect for couples who want to collaborate on their finances, manage shared expenses, and work towards financial goals as a team.

Features of Honeydue budgeting app

Honeydue has many features to consider but here are some top features of the Honeydue app:

Shared Financial Overview

Honeydue app allows couples to link and view all their financial accounts—bank accounts, credit cards, loans, and investments, in one place for easy tracking.

Customizable Privacy Settings

In Honeydue app partners can choose what financial information to share with their partner, keeping some accounts or transactions private while maintaining transparency on shared expenses.

Split Expenses

Honeydue app makes it simple to divide shared costs like rent, groceries, or utilities, ensuring fairness and reducing conflicts between couples.

In-App Chat

Honeydue app includes a built-in messaging feature, so that couples can discuss finances, bills, or transactions directly within the app.

This is the interface of Honeydue app

Best for

Honeydue app is perfect for couples who want to collaborate on their finances, manage shared expenses, and work towards financial goals as a team.

Rocket money budgeting app is one of the best budgeting apps as it has the main advantage of Bill Negotiation service. Rocket Money, formerly known as Truebill, is a personal finance app designed to help users to manage their subscriptions, track their spending, and save money effortlessly. The app connects to your bank accounts and credit cards, automatically identifying recurring subscriptions like streaming services, gym memberships, and software. It alerts you about any hidden fees, helps you cancel unwanted subscriptions, and even negotiates bills on your behalf (for a fee). Rocket Money also provides budgeting tools, goal tracking, and insights into your spending habits, making it easier to stick to a budget and save money.

Features of Rocket money

Rocket Money offers several features over other personal finance apps which makes it a strong choice for users looking to manage their money effectively.

Subscription Management

Rocket Money app automatically identifies and tracks recurring subscriptions, helping you spot any unwanted or forgotten services. This makes it easier to cancel subscriptions and save money without sifting through your bank statements.

Bill Negotiation

One unique feature is the ability to negotiate bills for you, such as cable or internet services. Rocket Money’s team works to lower your bills, which can save you significant money over time.

Automated Savings

The Rocket money app can help you to set up automatic savings by rounding up your purchases and saving the spare change or by scheduling recurring deposits, making saving effortless.

Custom Alerts

It sends alerts for unusual charges or bills, helping you stay on top of your expenses and avoid hidden fees. You can also receive reminders for upcoming bills, reducing the risk of late payments.

This is an interface of Rocket money app

Best for

It’s ideal for anyone looking to take control of their finances and eliminate unnecessary expenses.

Pricing

Free Plan:

The basic version of the app is free and includes features like tracking subscriptions, spending insights, and budgeting tools.

Premium Plan:

The premium plan, which costs around $3.00 to $12.00 per month (pricing may vary), unlocks additional features such as:

Simplifi as its name specifies, is the best budgeting app, designed to help users manage their money more effectively by offering a comprehensive, user-friendly platform for budgeting, tracking spending, and planning for financial goals. It connects to your bank accounts, credit cards, and investment accounts to give you a clear view of your finances.

Features of simplifi

Here are some important features of the Simplifi app:

Customizable Budgeting

Simplifi app allows you to set personalized budgets based on your income and spending patterns, giving you complete control over your financial goals.

Real-Time Transaction Tracking

Simplifi app automatically syncs with your bank accounts, credit cards, and investment accounts to track transactions in real-time, ensuring you stay up-to-date on your spending.

Cash Flow Forecasting

Simplifi offers cash flow forecasting to help you predict future spending and plan ahead for upcoming expenses.

Secure and Private

Simplifi uses bank-grade encryption to keep your financial data secure and private.

This is an interface of Simplify app

Best for

Simplifi is designed to make managing your finances simple and efficient, with a focus on clarity, customization, and real-time tracking.

Pricing

Free Trial: Simplifi provides a 30-day free trial so you can explore all its features before committing to paid plna.

Paid Plan: After the trial, the cost is approximately $5.99 per month or $47.75 per year if you choose the annual subscription.

GoodBudget is a simple, envelope-style budgeting app that helps users plan their spending and save money. It follows the traditional cash-envelope system, where you allocate specific amounts to different spending categories (like groceries, entertainment, etc.) each month. The app allows you to manually track your income and expenses, set savings goals, and create both short-term and long-term budgets. Unlike apps that sync with bank accounts, GoodBudget operates on a manual input system, which encourages users to be more mindful of their spending.

Features of GoodBudget app

Here are some important features of the GoodBudget app:

Envelope Budgeting System

Uses the traditional envelope method to allocate funds to different categories (e.g., groceries, savings, entertainment), helping you stay within budget.

Manual Transaction Tracking

Allows you to manually track income and expenses, giving you full control over your financial records.

Multiple Devices Sync

Syncs your budget across multiple devices, allowing you and your partner or family members to stay on the same page with shared budgets.

Cash Flow Management

Tracks both income and expenses to ensure you stay within your set budget, making it easy to see your remaining balances in each category.

Debt Tracking

Lets you track and manage your debt payments to help you stay on top of your financial obligations.

This is the interface of GoodBudget app

Best for

GoodBudget is a great choice for people who prefer a manual, hands-on approach to budgeting and want to manage their finances without automatic bank syncing.

Pricing

Free lifetime plan available with limited features. Premium also available which starts from 10$ per month or 80$ yearly.

The best budgeting app depends on your financial goals and personal preferences. Whether you are a seasoned budgeter or just starting out, these apps offer a range of features to help you achieve financial success in 2025. Start exploring today and take control of your financial future!

“Financial freedom is the state of having sufficient personal wealth to live comfortably without being dependent on a paycheck or active income to meet your financial needs, allowing for flexibility and the pursuit of life goals without financial stress.”

Financial freedom means having enough money to cover your living expenses, handle emergencies, and live with your goals without relying on a paycheck or debt. It’s the ability to live your life according to your choice without financial constraints. In simple terms, it’s when your money works for you, giving you peace of mind and control over your future.

Achieving financial freedom is a journey that involves careful planning, discipline, and smart financial decisions. Here’s a detailed breakdown of everything you need to know and do to master financial freedom.

Understanding Financial Freedom

Financial freedom isn’t about being rich; it’s about having control over your money and life. If you can meet your needs, handle emergencies, and pursue goals without constant stress over finances, it means you are financially free.

Flexibility: Freedom to make choices that prioritize your happiness.

Independence: No reliance on debt or paycheck-to-paycheck living.

The Core Pillars of Financial Freedom

a. Budgeting and Spending Wisely

Budgeting is the backbone of financial freedom. A budget is a plan that helps you direct your money toward your goals. It ensures you are living according to you and saving for the future as well.

Steps to Budget Effectively:

Track your spending: Monitor every expense for a month using apps like Mint or Excel.

Categorize expenses: Divide your expenses into needs (rent, groceries), wants (entertainment), and savings.

Use budgeting methods:

50/30/20 rule: Allocate 50% of your income to needs, 30% to wants, and 20% to savings.

Zero-based budgeting: Assign every dollar a job, ensuring income minus expenses equals zero.

Tips for Spending Wisely:

Shop with a list to avoid impulse purchases.

Use cash-back apps and loyalty programs for savings.

Avoid lifestyle inflation—don’t increase spending just because you earn more.

b. Saving Consistently

Saving is important for emergencies, goals, and building wealth. Without savings, unexpected events can lead to debt or financial instability.

Types of Savings to Focus On:

Emergency Fund:

Start with $1,000, then aim for 3–6 months of living expenses.

Use high-yield savings accounts to earn better interest.

Short-Term Goals:

Save for vacations, weddings, or a new car.

Consider separate savings accounts for each goal.

Long-Term Goals:

Build funds for retirement, buying a house, or your child’s education.

Automate Savings:

Set up automatic transfers to your savings account such as credit cards to ensure consistency.

c. Reducing and Eliminating Debt

Debt is one of the biggest barriers to financial freedom. High-interest debt can snowball, making it harder to save or invest.

Steps to Reduce Debt:

List all debts: Include interest rates, monthly payments, and total owed.

Choose a repayment method:

Snowball Method: Pay off the smallest debts first for quick wins.

Avalanche Method: Focus on high-interest debts first to save on interest.

Negotiate with lenders:

Ask for lower interest rates or consolidate debt into a single loan with better terms.

Avoid new debt:

Use cash or debit cards instead of credit cards.

Build an emergency fund to avoid using credit in emergencies.

d. Investing Wisely

Investing is how your money works for you, creating wealth over time. The earlier you start, the more you benefit from compound interest.

Investopedia, NerdWallet, and financial planning blogs.

Apps:

YNAB, Mint, Robinhood, Stash.

Steps to Start Today to gain financial freedom:

Assess your financial health.

Create a detailed budget.

Set clear, actionable goals.

Save consistently and start investing.

Stay disciplined and review progress regularly.

The Ultimate Goal to achieve financial freedom

Financial freedom empowers you to live life on your terms, free from financial stress. It’s about creating a future where money supports your dreams instead of holding you back. Start small, stay consistent, and take control of your financial future!

What is financial freedom formula?

Passive Income ≥ Living Expenses

This means your income from passive sources (like investments, rental properties, or dividends) should be enough to cover your essential and discretionary living expenses.

Steps to Build Toward Financial Freedom Using the Formula:

Calculate Your Living Expenses:

Include all monthly expenses (rent, utilities, groceries, insurance, entertainment, etc.).

Don’t forget irregular expenses like vacations or emergencies.

Build Passive Income Streams:

Invest in assets that generate income, such as:

Dividend-paying stocks

Real estate rentals

Peer-to-peer lending

Royalties from creative works (books, courses, etc.)

Grow Your Investments:

Use compounding to increase your wealth through consistent saving and investing.

Leverage retirement accounts like a 401(k) or IRA for long-term financial security.

Reduce Expenses:

Optimize your budget to lower unnecessary spending, increasing your savings rate.

Eliminate Debt:

Pay off high-interest debts to free up more money for saving and investing.

Achieve the Balance:

Once your passive income meets or exceeds your living expenses, you have achieved financial freedom.

Detailed Roadmap to Financial Freedom:

Achieving financial freedom requires a clear plan and consistent effort. Below is a comprehensive roadmap to guide you toward financial independence.

1. Define What Financial Freedom Means to You

Financial freedom looks different for everyone. Start by defining your goals:

Do you want to retire early?

Do you want to travel the world?

Do you want to spend more time with family or start your dream business?

Action:

Write down your short-term, mid-term, and long-term financial goals.

Determine how much money you’ll need to achieve these goals.

2. Assess Your Current Financial Situation

Understanding where you stand is crucial for building a plan.

Steps:

Calculate your net worth: Net Worth = Assets (savings, investments, property) – Liabilities (debts).

Track your income and expenses for a month to identify spending patterns.

Tools:

Use apps like Mint or Personal Capital to simplify tracking.

3. Create a Realistic Budget

A budget helps you control your spending and allocate funds toward savings and investments.

Allocate every dollar of income to a specific purpose until your budget balances at zero.

Action:

Regularly review and adjust your budget to align with your goals.

4. Build an Emergency Fund

An emergency fund is essential for financial security, protecting you from unexpected expenses like medical bills or car repairs.

Steps:

Start with $1,000 as a beginner goal.

Gradually save 3–6 months of living expenses.

Keep it in a high-yield savings account for easy access.

5. Eliminate High-Interest Debt

Debt, especially high-interest debt like credit cards, can derail your financial freedom plan.

Strategies:

Debt Snowball Method:

Pay off the smallest debts first for quick wins while making minimum payments on larger debts.

Debt Avalanche Method:

Pay off debts with the highest interest rates first to save on interest.

Action:

Stop accumulating new debt by using cash or debit cards for purchases.

6. Save and Invest Consistently

Saving and investing are the cornerstones of financial freedom. Savings provide security, while investments grow your wealth.

a. Save Regularly

Automate savings to ensure consistency.

Use separate accounts for different goals (e.g., emergency fund, vacations, down payment).

b. Invest Wisely

Start with low-risk, diversified investments like index funds or ETFs.

Contribute to retirement accounts:

Employer-sponsored 401(k) with matching.

Individual Retirement Accounts (IRAs) or Roth IRAs.

Explore passive income opportunities like rental properties or dividend stocks.

Tip: Start early to maximize the power of compound interest.

7. Create Multiple Income Streams

Relying on a single source of income can limit your progress. Diversifying your income accelerates your journey to financial freedom.

Ideas:

Side Hustles:

Freelance work, consulting, blogging, or selling handmade items.

Passive Income:

Dividend-paying stocks, rental properties, royalties from digital products.

Upskill for Higher Income:

Invest in education or certifications to qualify for higher-paying roles.

8. Protect Your Wealth

Safeguarding your financial progress is critical.

How to Protect Yourself:

Insurance:

Health, life, property, and disability insurance for risk mitigation.

Estate Planning:

Create a will, set up a trust, and assign beneficiaries for your accounts.

Emergency Fund:

Maintain liquidity for unforeseen expenses.

9. Plan for Retirement

Retirement planning ensures you can sustain your lifestyle even when you’re no longer working actively.

Steps:

Estimate how much you’ll need in retirement (e.g., 70–80% of your pre-retirement income).

Use retirement accounts:

401(k), IRA, or Roth IRA.

Solo 401(k) or SEP IRA for self-employed individuals.

Invest consistently in diversified portfolios.

Tip: Use online retirement calculators to set savings targets.

10. Continuously Educate Yourself

Financial literacy is a lifelong skill that helps you make smarter decisions.

11. Monitor Your Progress

Regularly evaluate your financial plan to ensure you’re on track.

How to Monitor:

Review your budget monthly.

Track net worth growth quarterly.

Reassess your goals annually and adjust plans as needed.

12. Achieve Financial Freedom

When your passive income covers your living expenses, you’ve achieved financial freedom. At this stage:

Focus on maintaining and growing your wealth.

Pursue your passions and goals without financial constraints.

what is the difference between financial freedom and financial independence

The terms financial freedom and financial independence are often used interchangeably, but they have subtle differences based on context and perspective. Here’s a breakdown to clarify:

Financial Independence

Definition: Financial independence is the state of having enough wealth or income to cover your basic living expenses without needing to work actively. It often means your passive income (from investments, rentals, etc.) meets or exceeds your essential expenses.

Key Focus:

Self-sufficiency and security.

Eliminating dependency on a paycheck or others (e.g., family or government aid).

Covering basic needs without financial worry.

Goal:

Achieving financial independence is often viewed as a milestone toward financial freedom.

Example: Someone who has enough in savings, investments, or passive income to pay for their housing, food, and utilities without working a job is financially independent.

Financial Freedom

Definition: Financial freedom is a broader concept that includes financial independence but goes beyond just meeting basic needs. It’s about having the ability to make life choices without financial constraints, such as pursuing passions, traveling, or retiring early.

Key Focus:

Flexibility and lifestyle.

The ability to afford not just needs but also wants and personal aspirations.

Freedom from financial stress and obligations like debt.

Goal:

Financial freedom represents the ultimate state where money no longer dictates life decisions.

Example: Someone who can afford to retire early, travel the world, and pursue hobbies without worrying about running out of money is financially free.

Key Differences

Aspect

Financial Independence

Financial Freedom

Scope

Focuses on meeting basic needs.

Includes independence but extends to fulfilling wants and goals.

Income Level

Passive income equals essential expenses.

Passive income exceeds expenses, allowing lifestyle choices.

Dependency

No reliance on a job or external support.

Complete freedom from financial constraints or stress.

Mindset

Security and self-sufficiency.

Empowerment and flexibility.

Goal

A stepping stone.

The ultimate financial goal.

In Practice

Financial independence might mean you can stop working a traditional 9-to-5 job and survive on your savings and investments.

Financial freedom means you can not only stop working but also afford to live life on your terms, such as traveling, starting a passion project, or donating generously to causes you care about.

Both are interconnected, and achieving financial independence is often a necessary step on the path to financial freedom.

What is Absolute Financial Freedom?

Absolute financial freedom is the ultimate state of financial independence where you have complete control over your life without any financial limitations or worries. It means having enough wealth and passive income to not only cover all your basic needs and lifestyle expenses but also pursue your dreams, passions, and goals without ever being constrained by money.

Characteristics of Absolute Financial Freedom

Unlimited Lifestyle Choices:

You can live where you want, travel when you want, and do what you love without considering the cost.

Example: Choosing to retire early, travel the world, or fund large-scale philanthropic projects.

No Financial Stress:

Money is no longer a source of worry, whether for emergencies, bills, or long-term planning.

Example: Being unaffected by market downturns because of robust wealth management.

Complete Independence:

No reliance on a job, loans, or financial support from others.

Example: Living entirely off passive income streams like investments, royalties, or rental properties.

Excessive Wealth Beyond Needs:

Your wealth significantly exceeds your current and future needs, allowing for luxuries, investments, and unexpected expenses without denting your financial stability.

Example: Owning multiple properties, funding children’s education, and still having a surplus.

Flexibility to Take Risks:

You can explore risky ventures, creative pursuits, or start new businesses without fear of losing your financial stability.

Example: Starting a new business purely out of passion without worrying about its profitability.

How Absolute Financial Freedom Differs from Financial Freedom

Aspect

Financial Freedom

Absolute Financial Freedom

Wealth Level

Covers your desired lifestyle and goals.

Far exceeds all conceivable needs and desires.

Risk Tolerance

Moderate; still mindful of preserving wealth.

High; can afford significant financial risks.

Security vs. Excess

Focuses on security and comfort.

Emphasizes abundance and luxury.

Example

Retiring comfortably with passive income.

Retiring as a millionaire or billionaire with unlimited options.

Steps to Achieve Absolute Financial Freedom

Set Lofty Financial Goals:

Identify how much wealth would allow you to live with no limits (e.g., $10 million, $50 million).

Define what “absolute” means to you (luxury, philanthropy, etc.).

Create High-Impact Income Streams:

Build multiple streams of income, focusing on scalable sources like businesses, high-value investments, or intellectual property.

Example: Investing in real estate, startups, or creating a globally successful product.

Maximize Investments:

Invest aggressively in high-growth assets (stocks, real estate, businesses).

Diversify to include stable income sources like bonds and dividends for security.

Optimize Tax Efficiency:

Work with financial advisors to reduce tax liabilities and retain more of your wealth.

Example: Use trusts, offshore accounts, or legal tax havens.

Focus on Exponential Wealth Creation:

Look for opportunities with massive returns (e.g., venture capital, cryptocurrency, IPOs).

Example: Invest early in disruptive technologies or industries.

Protect and Grow Wealth:

Use insurance, estate planning, and legal strategies to safeguard assets.

Continuously reinvest profits to generate compounding returns.

Who Achieves Absolute Financial Freedom?

Absolute financial freedom is typically achieved by:

Entrepreneurs who sell businesses for significant profits.

Investors with portfolios generating multi-million-dollar returns.

Inheritors of generational wealth who grow it responsibly.

High-income professionals who save, invest, and diversify effectively.

In Summary: Absolute financial freedom is the pinnacle of financial success where money is no longer a factor in any decision you make. It represents the ability to live abundantly, take risks, and leave a lasting impact while enjoying total peace of mind about your financial future.

what is houston financial freedom?

Houston Financial Freedom refers to achieving financial independence and stability while living in Houston, Texas, or a specific program, organization, or event aimed at promoting financial literacy and independence in that region.

If you’re referring to a general concept, achieving financial freedom in Houston might involve tailoring strategies to the cost of living, job opportunities, and investment options in the area. If it’s a specific entity like a business or nonprofit, it could be focused on helping individuals manage debt, invest, or plan for financial independence.

General Path to Financial Freedom in Houston

Understand Houston’s Cost of Living:

Houston has a relatively affordable cost of living compared to other major U.S. cities. Housing is a significant factor, so financial freedom might involve owning or renting in a cost-effective neighborhood.

Leverage Houston’s Job Market:

Houston’s economy thrives on industries like energy, healthcare, and technology. Aligning your career with high-demand sectors can accelerate income growth.

Utilize Local Resources:

Seek out local financial advisors, workshops, or community resources designed to boost financial literacy.

Invest in Real Estate:

Houston’s real estate market can be an excellent opportunity for passive income through rentals or property flipping.

How to Achieve Financial Freedom Before 30: A Detailed Guide

Achieving financial freedom before the age of 30 may seem ambitious, but it’s entirely possible with the right strategy, discipline, and mindset. Financial freedom at this age means having enough wealth to live comfortably without relying on a traditional 9-to-5 job or active income. Here’s a detailed roadmap on how to achieve it:

1. Define Your Vision of Financial Freedom

Step 1: Clarify Your Goals Before diving into the specifics, define what financial freedom means for you:

Do you want to retire early?

Do you want to travel the world without worrying about money?

Do you want to own your dream home or start a business?

Action:

Write down your personal, lifestyle, and financial goals.

Quantify your target amount of passive income and wealth.

2. Build a Strong Foundation with Financial Literacy

Step 2: Master Basic Financial Concepts Understanding key financial principles is essential to making smart decisions about your money. Some areas to focus on:

Budgeting: Track your income and expenses to understand where your money goes.

Debt Management: Learn how to eliminate high-interest debt (e.g., credit cards).

Investing: Start learning about different investment vehicles (stocks, bonds, real estate, etc.).

Saving: Learn the importance of an emergency fund and saving for specific goals.

Action:

Read books like The Millionaire Next Door by Thomas Stanley, Rich Dad Poor Dad by Robert Kiyosaki, and The Intelligent Investor by Benjamin Graham.

Listen to financial podcasts and follow credible blogs to stay updated.

3. Minimize and Eliminate Debt

Step 3: Pay Off High-Interest Debt Debt is one of the biggest obstacles to financial freedom. High-interest debt, like credit card debt, can hinder your ability to save and invest. Eliminate it as quickly as possible.

Debt Repayment Strategies:

Debt Snowball: Pay off the smallest debt first to build momentum, then move on to larger debts.

Debt Avalanche: Focus on paying off the debt with the highest interest rate first.

Action:

Aim to eliminate all high-interest debt by year one.

Avoid accumulating new debt by living within your means.

4. Increase Your Income Streams

Step 4: Maximize Earning Potential Relying solely on a job may limit your income. To achieve financial freedom faster, it’s essential to create additional income streams.

Ideas for Increasing Income:

Side Hustles: Start freelancing, offer consulting services, or sell products online.

Start a Business: Launch a small business that can scale. Many successful entrepreneurs start businesses in their 20s that grow rapidly.

Investing: Invest in stocks, real estate, or dividend-paying assets to build passive income.

Action:

Identify your skills and interests, then look for ways to monetize them.

Invest a portion of your earnings into assets that generate passive income.

5. Live Below Your Means

Step 5: Practice Frugality and Smart Spending To accumulate wealth, you must save and invest a significant portion of your income. One of the best ways to achieve this is by living below your means. This doesn’t mean depriving yourself but being mindful of unnecessary spending.

Key Areas to Cut Back:

Housing: Consider renting in an affordable area or getting a roommate to save on rent.

Transportation: Drive a used car or use public transportation to avoid expensive monthly car payments.

Lifestyle: Avoid lifestyle inflation by not increasing your spending as your income increases. Continue to live frugally even when you get raises or promotions.

Action:

Follow the 50/30/20 rule: 50% for needs, 30% for wants, and 20% for savings and investments.

Save at least 50% of your income if possible.

6. Invest Early and Consistently

Step 6: Make Your Money Work for You The earlier you start investing, the more time your money has to grow through the power of compounding. Start with low-cost index funds, ETFs, or target-date funds for diversified, long-term growth.

Investment Strategies:

Stock Market: Invest in index funds or low-fee ETFs that track the overall market.

Real Estate: Consider investing in real estate for passive rental income or capital appreciation.

Dividend Stocks: Invest in stocks that pay dividends, which can be reinvested or used as passive income.

Action:

Start contributing to tax-advantaged accounts like a 401(k), Roth IRA, or Traditional IRA.

Automate your investments so that they happen consistently, even if it’s a small amount.

7. Build Passive Income Streams

Step 7: Diversify Your Income While active income is necessary, passive income is what enables financial freedom. You need to build income sources that generate money with little active involvement.

Types of Passive Income:

Rental Income: Buy rental properties that provide consistent monthly cash flow.

Dividends: Invest in dividend-paying stocks or funds that provide regular payouts.

Online Businesses: Create an online business (blog, digital products, affiliate marketing) that earns money while you sleep.

Action:

Start small by investing in stocks or real estate.

Reinvest your passive income to build larger income streams over time.

8. Save for Emergencies and Big Purchases

Step 8: Build an Emergency Fund Financial freedom doesn’t mean living without a safety net. Having an emergency fund of 3-6 months of living expenses ensures that unexpected costs won’t derail your financial goals.

Action:

Save at least $1,000 to start, then gradually build up to 3-6 months of living expenses.

Keep your emergency fund in a high-yield savings account for easy access and some interest growth.

9. Monitor Your Progress and Adjust

Step 9: Review and Adjust Regularly Achieving financial freedom requires regular assessment and adjustment. Track your net worth, monitor your spending, and make sure your investments are on track.

Action:

Review your financial situation at least quarterly.

Reassess your goals annually and adjust strategies as needed.

10. Cultivate a Growth Mindset

Step 10: Stay Committed and Patient Achieving financial freedom at a young age requires a mindset of delayed gratification and long-term planning. There will be setbacks, but maintaining discipline, learning from mistakes, and staying focused on your goals is crucial.

Action:

Surround yourself with like-minded individuals who support your financial goals.

Continuously educate yourself on personal finance, investing, and wealth-building strategies.

Conclusion

Achieving financial freedom before 30 is ambitious but attainable with discipline, strategic planning, and smart decisions. By focusing on increasing your income, investing early, minimizing debt, and practicing frugality, you can position yourself to retire early or enjoy financial independence and live life on your terms. Start today, and every decision you make will bring you one step closer to the freedom you desire!

To know more about financial education visit our website.

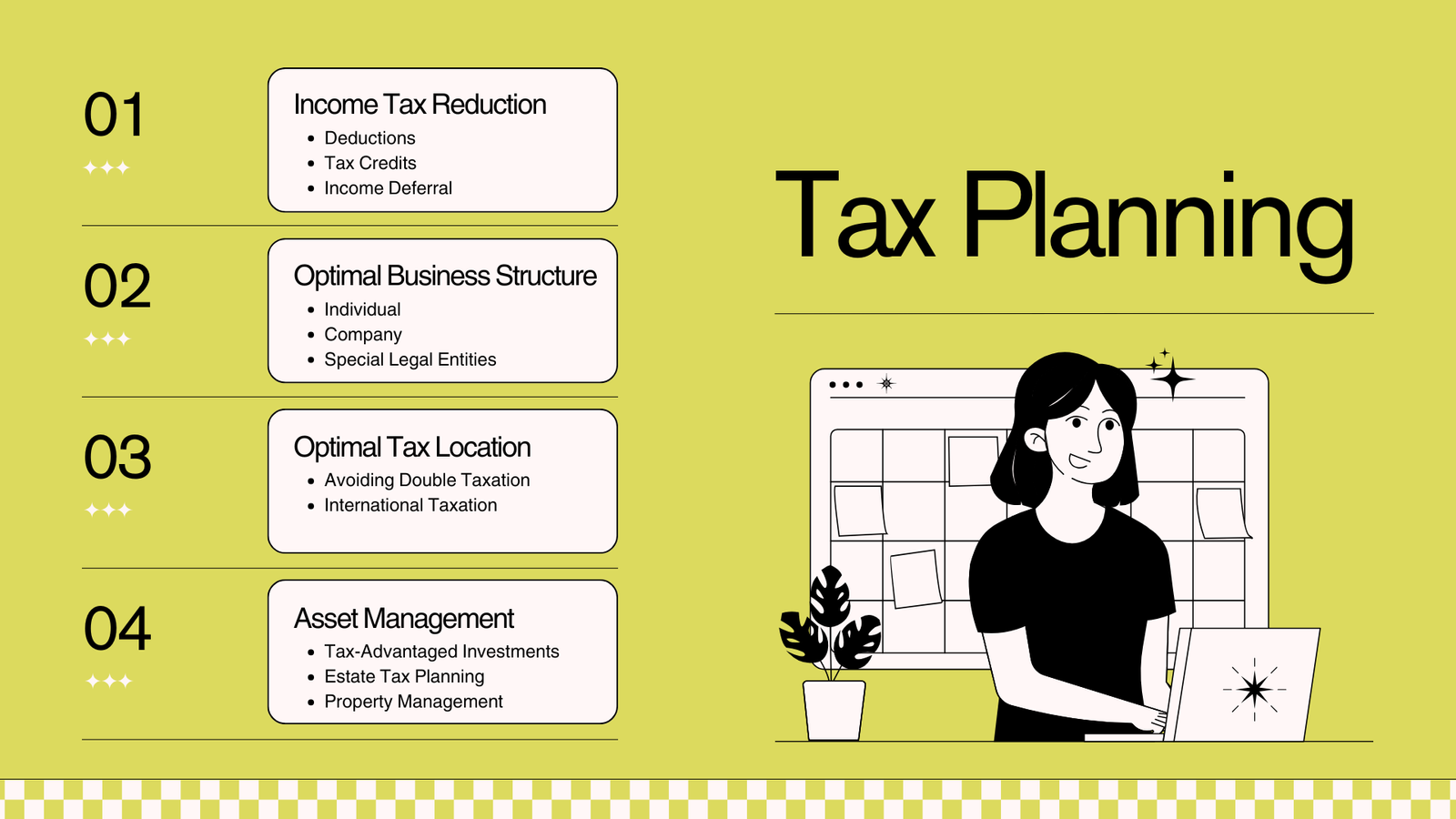

Tax planning is the process of organizing your finances in a way that minimizes the amount of tax you have to pay, all within the legal framework. This approach allows you to maximize your savings and use your money more effectively. Tax planning can sound complex, but in simple terms, it’s about making the most of tax deductions, credits, and tax-efficient investments to keep more of your income.

Why is Tax Planning Important?

Tax planning is crucial for several reasons:

Maximizing Savings: By taking advantage of available tax benefits, you can reduce your tax burden, leaving you with more disposable income. This money can be reinvested, saved, or used to fund personal goals, like travel, education, or retirement.

Achieving Financial Goals: Effective tax planning aligns with your broader financial objectives, such as saving for a home, funding education, or building retirement savings. With good planning, you can reach these goals sooner.

Staying Legally Compliant: Following tax laws carefully ensures that you don’t face penalties or legal issues. Tax planning helps you remain compliant while benefiting from legal tax-saving opportunities.

Reducing Tax Liability: Tax planning focuses on reducing the taxes you owe, allowing you to enjoy more of your earnings. This is achieved through strategic decisions about deductions, credits, and investment choices.

Key Components of Tax Planning

To understand tax planning, it’s important to look at the main strategies used to lower taxable income and, in turn, tax liability. Here are some of the most common elements:

Income Management: The way and timing in which you receive your income can have an impact on the taxes you owe. For instance, you might defer a bonus to the next tax year if it keeps you in a lower tax bracket, reducing the overall tax you’ll pay.

Investments: Certain investments provide tax benefits. For instance, investing in tax-saving bonds, mutual funds, or retirement accounts can lower your taxable income. In some cases, you may earn tax-free interest or get tax deductions for contributions to retirement plans. To learn more about maximizing retirement savings, check out Fidelity’s retirement planning page.

Deductions and Credits: Tax deductions lower your taxable income, while tax credits directly reduce the amount of tax you owe. Examples of deductions include those for mortgage interest, charitable contributions, and student loan interest. Credits might include those for education expenses, dependent care, and energy-efficient home improvements.

Types of Tax Planning

Tax planning strategies vary depending on your financial situation, goals, and the time frame you’re considering. Here are four main types of tax planning:

Short-term Tax Planning: This involves strategies that apply within the current tax year, aiming to reduce your tax burden quickly. For example, you might invest in tax-saving schemes or claim available deductions and credits by year-end.