Did you know that 40% of Americans can’t cover a $400 emergency expense? If that statistic makes you nervous, you’re not alone. Life is full of surprises—some good, some not so good—and having a financial safety net can mean the difference between weathering a storm and being swept away.

But here’s the thing: not all savings are created equal. An Emergency fund vs savings serve different purposes and understanding the difference is key to building a solid financial foundation. In this guide, we’ll break down what sets them apart, why you need both, and how to get started.

What is an emergency fund?

An emergency fund is a dedicated pool of money set aside specifically for unexpected expenses. Think of it as your financial safety net for life’s curveballs, such as:

- Medical emergencies

- Car repairs

- Job loss

- Home repairs

How much should you save?

Financial experts recommend saving 3-6 months’ worth of living expenses in your emergency fund. This ensures you’re prepared for major disruptions without derailing your long-term goals.

What are general savings?

General savings, on the other hand, are funds you set aside for planned expenses or personal goals. These could include:

- A dream vacation

- A down payment on a house

- A new car

- A wedding or other big life event

Unlike an emergency fund, general savings are meant for things you can anticipate and plan for.

Key differences between an Emergency fund vs savings

| Aspect | Emergency Fund | General Savings |

|---|---|---|

| Purpose | Covers unexpected expenses | Funds planned goals or purchases |

| Amount | 3-6 months of living expenses | Varies based on your goals |

| Accessibility | Easily accessible (e.g., savings account) | Can be less liquid (e.g., CDs, bonds) |

| Priority | High (financial safety net) | Lower (after emergency fund is funded) |

Why you need both

Here’s the truth: an emergency fund vs savings serve different but equally important roles in your financial life.

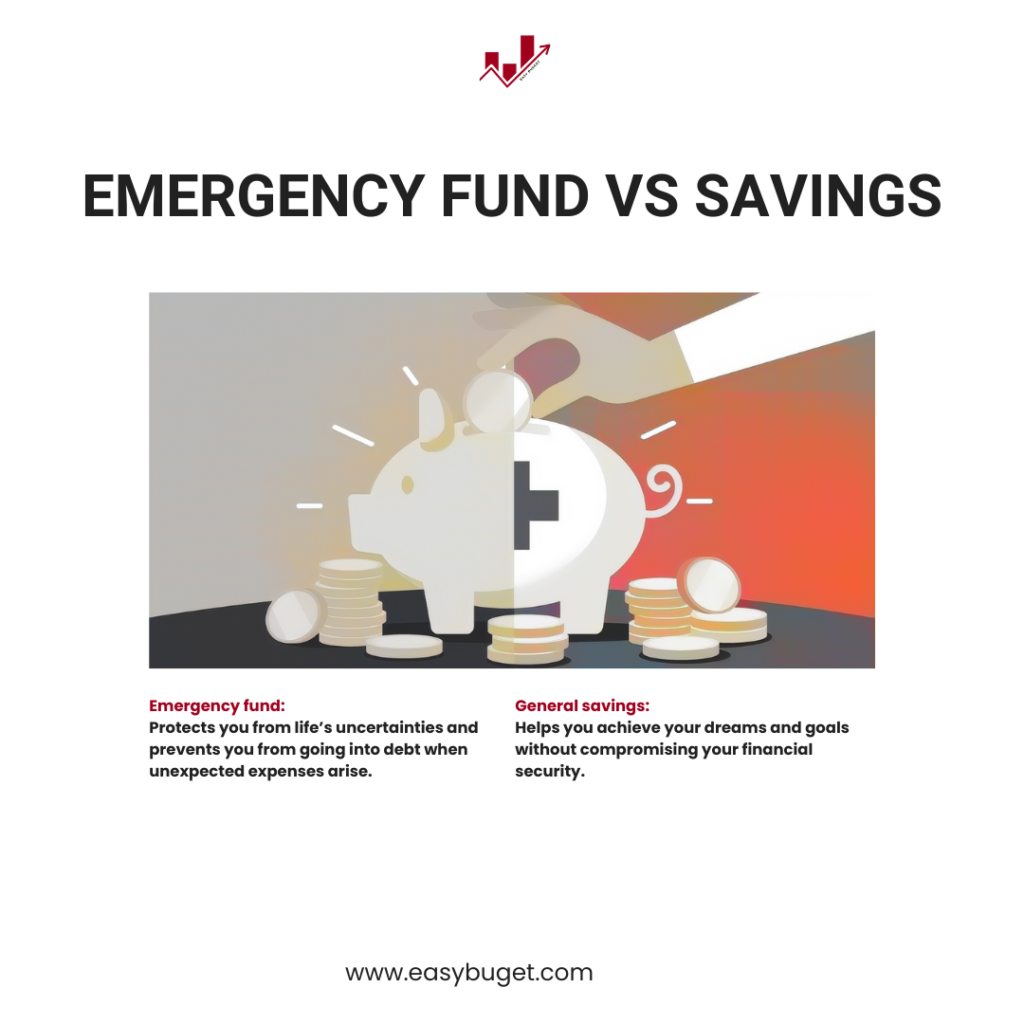

- Emergency fund: Protects you from life’s uncertainties and prevents you from going into debt when unexpected expenses arise.

- General savings: Helps you achieve your dreams and goals without compromising your financial security.

Without both, you’re either risking financial instability or missing out on opportunities to grow and enjoy your money.

How to build an emergency fund

Building an emergency fund might seem daunting, but it’s easier than you think. Here’s how to get started:

- Set a goal: Aim for $1,000 initially, then work toward 3-6 months of living expenses.

- Automate savings: Set up automatic transfers to your emergency fund each payday.

- Cut expenses: Identify non-essential spending (e.g., dining out, subscriptions) and redirect that money to your fund.

- Use windfalls: Allocate bonuses, tax refunds, or gifts to boost your savings.

- Keep it accessible: Store your emergency fund in a high-yield savings account for easy access and growth.

How to grow your general savings

Once your emergency fund is in place, it’s time to focus on your general savings. Here are some tips:

- Set clear goals: Define what you’re saving for and how much you need.

- Create a budget: Track your income and expenses to identify areas where you can save more.

- Use the right tools: Consider high-yield savings accounts, CDs or investment accounts for long-term goals.

- Pay yourself first: Treat savings like a bill and prioritize it in your budget.

- Celebrate milestones: Reward yourself when you hit savings goals to stay motivated.

Common mistakes to avoid

Even with the best intentions, it’s easy to make mistakes when managing your savings. Here’s what to watch out for:

- Using your emergency fund for Non-Emergencies: That tropical vacation can wait—your emergency fund is for true emergencies only.

- Not prioritizing an emergency fund: Without one, you risk going into debt when unexpected expenses arise.

- Overlooking interest rates: Keep your savings in accounts that earn interest to maximize growth.

- Saving without a plan: Set clear goals and timelines to stay on track.

FAQs About Emergency funds vs savings

1. How much should I have in my emergency fund?

Aim for 3-6 months of living expenses, but start with a smaller goal like $1,000 if you’re just getting started.

2. Can I use my emergency fund for non-emergencies?

It’s best to avoid this. Your emergency fund is for true emergencies only.

3. Where should I keep my emergency fund?

A high-yield savings account is ideal—it’s easily accessible and earns interest.

4. How do I prioritize between saving for emergencies and other goals?

Focus on building your emergency fund first, then shift your attention to general savings.

Conclusion

An emergency fund vs savings are two sides of the same coin—both are essential for a healthy financial life. Your emergency fund protects you from the unexpected, while your general savings help you achieve your dreams and goals.

So, what’s your next step? Start by setting up an emergency fund if you don’t already have one, and then work toward your savings goals. Remember, every dollar you save today is a step toward a more secure and fulfilling tomorrow.

Call-to-Action:

- Do you have an emergency fund or general savings? Share your tips and experiences in the comments below!

- If you found this guide helpful, don’t forget to share it with your friends and family. Let’s help everyone build a stronger financial future!

Please subscribe Easy Budget to stay updated about our latest blogs!

1 thought on “Emergency fund vs savings in 2025: What’s the difference and why you need both”